The 12-12-12 rule – save for 12 years, live off the capital for life

A pedagogical mnemonic showing how compound interest can turn 12 years of monthly saving into a lifelong income. Here's how it works.

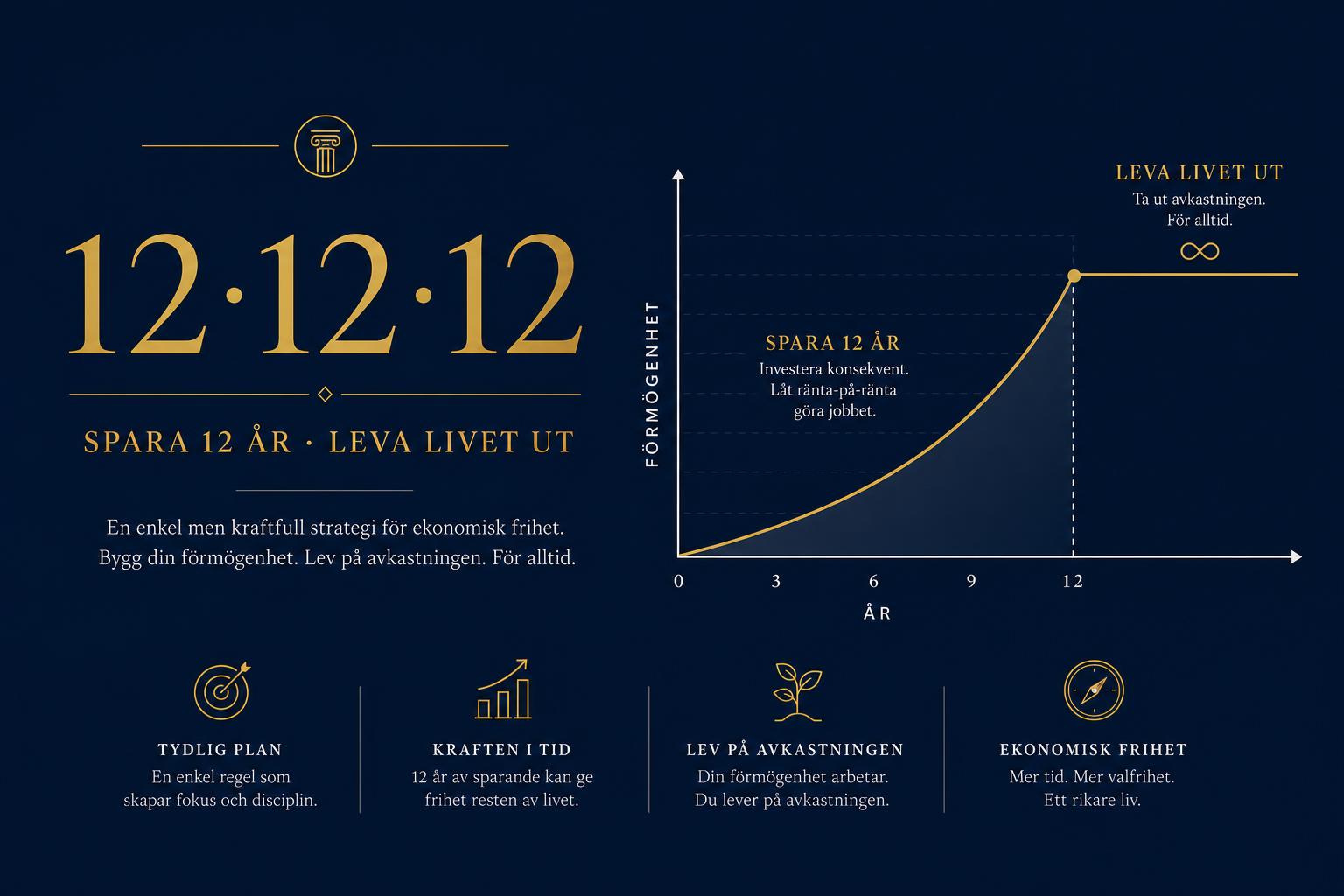

The 12-12-12 rule is a pedagogical mnemonic in personal finance that instantly illustrates the power of compound interest. The idea is simple: if you invest a chosen amount every month for 12 years, you will have built up a capital that allows you to withdraw the same amount every month for the rest of your life. Three twelves, one life of financial freedom.

Let's take a concrete example. Say you save 5,000 SEK per month in a broad equity fund. After twelve years you have deposited a total of 720,000 SEK. However, with an average real return of 7 per cent per year, the capital has grown to roughly 1.1–1.2 million SEK thanks to compound interest. That sum is large enough for the fund's continued return to cover a monthly withdrawal of 5,000 SEK forever – assuming the average return holds.

The rule therefore assumes that the stock market delivers a long-term real return of around 6.5–7 per cent, which is in line with historical global equity returns after inflation. The higher the return, the faster you reach the goal; at 5 per cent it takes somewhat longer, and at 8 per cent it goes considerably faster. It is this uncertainty that makes the rule a pedagogical thought experiment rather than a guaranteed life plan.

In practice, several things can affect the outcome. Inflation slowly erodes purchasing power, fund fees take a few tenths of a per cent each year, and taxes such as the Swedish ISK standard rate affect net withdrawals. Then there is sequence-of-returns risk – if the market drops sharply during your final saving years or shortly after you start withdrawing, the capital can fall more than expected. A buffer of a few years' expenses and a flexible withdrawal plan is therefore wise.

For those already familiar with the FIRE movement, the 12-12-12 rule is an elegant compression of the same principle. The FIRE number is built on 25 times annual expenses; the 12-12-12 rule says that twelve years of disciplined saving can be enough to match those same expenses forever. The difference is that the rule focuses on time rather than an absolute capital – and it makes it easier to understand why every monthly contribution actually matters.

The most important thing about the 12-12-12 rule is not to memorise it as an absolute truth, but to let it work as a thought experiment. Every thousand you invest today is not just a saving; it is a future monthly payout to yourself. The earlier you start, the more time the capital has to grow – and the sooner you reach the point where your money works for you instead of the other way around.

Try it yourself in the calculator below. Set monthly savings to the amount you can manage today, adjust the return to 7 per cent, and study how long it takes to reach a capital that pays back the same sum every month. Twelve years is shorter than you think.

FIRE calculator

Calculate your FIRE number

Results are in today's money – return is adjusted for inflation so the target stays realistic.

Goal (today's value)

7,500,000 $

Default FIRE number: 7,500,000 $

Years to FIRE

27.1

Real return: 4.90 %

Withdrawal at 4%

25,000 $/mo

300,000 $/yr

Nominal goal then: 12,815,821 $

Note: Simplified estimate. Real returns, inflation, taxes, and sequence-of-returns risk vary. None of this is financial advice.